Warner Bros Discovery: The stuff that multi-baggers are made of

How a spin-off merger created a fantastic pure-play media investment opportunity

Please subscribe for future content or follow me on Twitter (@moneyflowinvest) if you find this article valuable!

UPDATE: Please read Revisiting Warner Bros Discovery: A Tale of Ambitious Mergers, Market Realities, and Survival in the Streaming Era for the latest analysis.

Warner Bros Discovery ($WBD) is a global media and entertainment company that develops, produces, and acquires scripted and unscripted content such as blockbuster movies, tv shows, sports, and news networks. It monetizes these assets through distribution fees, advertisements, and content licensing. The conglomerate is the product of a long history of M&A transactions, including Discovery’s strategic acquisition of Scripps network in 2018 and the recent merger in April 2022 between WarnerMedia, a spin-out from AT&T, and Discovery.

While Netflix and Disney’s stocks have significantly dropped from their all-time highs, they still have a 14x and 42x EV (Enterprise Value) / EBIT multiple, respectively. On the other hand, the market values WBD as a dying cable company with an ~8 EV / EBIT1 multiple. This perspective is the wrong way to think about it. The newly formed Warner Bros Discovery has a prestigious brand, deep library of media assets, a fully scaled content generation machine, and a global reach that instantly catapults it into a market-leading position from sub-scale.

Shrouded by the fear of an industry slowdown amid Netflix losing 200k net subs in Q1 2022, the selloff of WBD is creating an unjustifiably cheap stock. Investors are simply not adequately accounting for WBD’s operating earnings expansion from $3B+ in synergies, leverage in affiliate fee negotiations, and DTC (direct-to-consumer) growth opportunities. Once the fog lifts through the execution of the business, investors will recognize the actual value of the underlying assets. I believe this will cause investors to rerate the stock to a higher multiple against a backdrop of elevated earnings and rapid deleveraging.

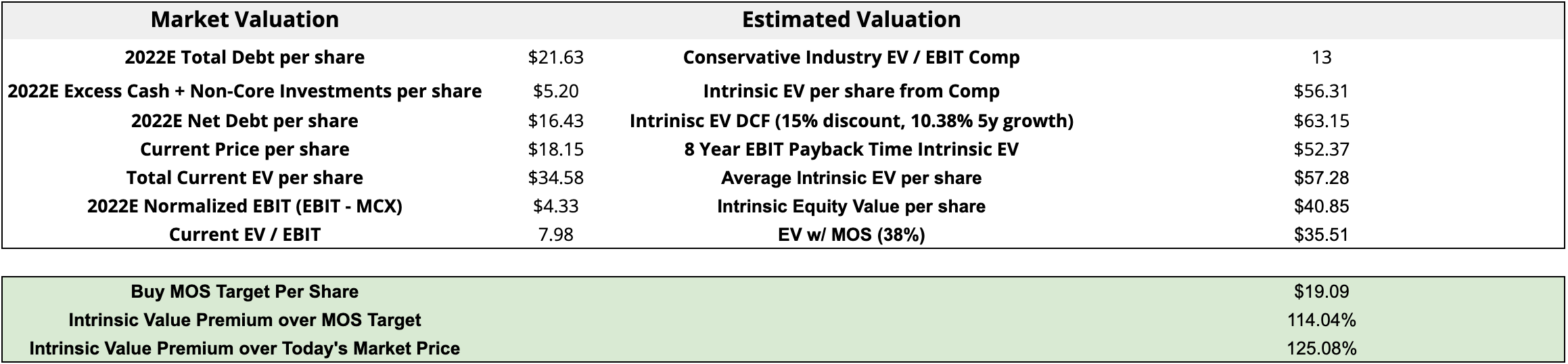

WBD is currently worth an equity value of at least $40.85 per share. With a substantial risk-adjusted MOS (Margin of Safety), my buy target price is ~$19 per share. The current market price of $18.15 is below this target. Purchasing the stock at this considerable discount unlocks a fantastic 125% growth opportunity. The current market share price provides an adequate margin of safety and downside protection for the following risks:

Leveraged Balance Sheet

Declining Linear2 Revenues

Content Spend Treadmill

WarnerMedia’s Global Expansion Limitation Until 2025

Management Execution Risk

The Visual Media Industry Landscape

The company is following the evolutionary trend of the media broadcasting industry, distributing content directly to the consumer through OTT or “over the top,” which means video content streamed over the internet instead of through legacy linear tv cable bundles. Netflix is the trailblazer for this online streaming format. Over the past decade, virtually every major media organization has followed suit. This paradigm shift has enabled companies to have direct relationships with the end consumers instead of relying on third-party MVPDs (Multichannel Video Programming Distributors) that have historically had those relationships.

Cord-cutting is on the other side of the coin of this secular direct-to-consumer trend as households are ditching their expensive cable bundles for streaming platforms. For example, Kagan projects traditional US multichannel revenue will decrease 28% from 2021 through 2025. In the S4 SEC document, management expects US and International linear revenues to reduce annually by 4% and 3% through the same period.

The decision to merge WarnerMedia with Discovery was an action that reflected the overall trend toward consolidation within the industry that is just beginning to ramp up. Achieving scale is crucial for businesses in the industry to win over enough customers and minimize churn. This reality means a company must possess a deep library and generate a steady stream of compelling content such as blockbuster films and binge-worthy shows. Furthermore, it needs enough revenue to spread across these large fixed costs to have a viable business model. Thus, M&A activity is the logical evolutionary step for media companies to survive. Other prominent M&A examples include Comcast’s acquisition of Sky, Disney’s takeover of 21st Century Fox, Viacom's merger with CBS, and Amazon’s $8.5 billion purchase of MGM studios.

Moats

WBD’s competitors include Netflix, Amazon, Disney, Paramount (formerly ViacomCBS), and Comcast (NBCUniversal). These staunch rivals all have their own DTC platforms. A subset also distributes content through other mediums. The company competes with other forms of media that vie for consumer attention, such as YouTube, video games, and social media platforms. While there are seemingly infinite ways that people can entertain themselves, WBD has two primary moats (brand and toll bridge moats) that keep audiences coming back and allow it to generate copious amounts of free cash flow. The two newly combined businesses have a > 30% Gross Margin on a pro forma basis, which suggests that they are separately able to demand a substantial premium for monetizing their media rights. Its durable competitive advantage continues to expand as it increases its bargaining power with advertisers, talent, and buyers. While the secular legacy cable business decline is a medium-term headwind, the shift to a direct relationship with the end customer and a higher-margin product is a fantastic long-term opportunity for WBD. Compared to Netflix, HBO Max and Discovery+ are less penetrated.

Toll Bridge Moat (Strong and growing)

A business with a toll bridge moat has substantial bargaining power with its suppliers or buyers. This dynamic often occurs when a company has a near-monopoly in its industry and its customers/partners have to go through them to access whatever they need.

Before merging, the companies had very different types of media. WarnerMedia has produced major blockbuster flicks such as “Harry Potter,” “Batman,” “Godzilla,” and “Lord of the Rings.” It also owns hit TV shows such as “Friends,” “The Sopranos, and “The Big Bang Theory.” On the other hand, Discovery is the leader in a niche market for unscripted shows produced by many TV networks such as the Discovery Channel, HGTV, Food Network, MotorTrend, and TLC. It also has a massive reach into 200+ countries worldwide and operates unique distribution feeds in nearly 50 languages. Once these complementary offerings fully consolidate into one DTC streaming platform, it will boast ~200k hours of video content replenished through ~$20 billion (and growing) in annual spending. The media conglomerate packs a powerful one-two punch with premium scripted and unscripted content (including long-term sports rights for the MLB, NHL, NBA, March Madness, the Olympics, and Tennis) that is difficult for its peers to match.

With such an extensive library and international localization presence, consumers will flock to WBD’s new DTC offering. Shortly after the deal closed, HBO Max had 76.8 million subs while Discovery had 24 million. Management noted that less than half of Discovery+ users subscribe to HBO Max (WarnerMedia’s brand). Assuming this amounts to a 40% overlap, the combined company will have over 90 million subs. In comparison, Netflix and Disney have ~222 million and ~130 million, respectively. While there is a lot of work to surmount its peers in sub count, potential customers on the fence about Discovery+ or HBO Max now have a much more appealing proposition to consider. The good news is that these subscriptions are not mutually exclusive. Households often subscribe to multiple streaming services (around four on average). Additionally, the average amount spent per household on cable is somewhere between $50-130 monthly, depending on various factors such as location, provider, and packages. In other words, it seems likely that there is room for WBD’s consolidated streaming service to be at the top of the list of every household with the amount of value that it provides.

While linear revenues are clearly on a downward spiral, the merger provides the business with tremendous negotiating leverage and pricing power when contracts expire. As it continues to scale up, the company has the clout to boost affiliate rates to help offset the MVPD subscriber losses. Discovery was already well-positioned to negotiate higher rates since it delivers close to 20% of total viewership for its linear affiliates and is a big player in the cable company space. It maintains this high viewership level since it engages customers with a diverse range of nutritional content. Additionally, churn is in the “low-single digits” as active viewing subscribers watch an average of three hours of content per day. The MVPDs require Discovery’s networks to hold onto their remaining audiences. Now that WarnerMedia has entered the fold, this becomes even more true.

Lastly, this positive pricing power dynamic also applies to rates it can charge its advertisers on the new streaming platform. According to management, WBD’s new DTC offering will have three tiers. These options include free/ad-heavy (AVOD), a cheap/ad-light, and a high premium/zero-ads (SVOD) tiers. The benefit of OTT distribution is that advertisers can precisely target consumers similar to the capabilities on YouTube or social media networks. Since many consumers will pay for SVOD, the amount of advertising space will be limited. The combination of an increasingly attractive advertising platform and limited supply should bode well for the rates that it charges. The CEO, David Zaslav, touched on this dynamic during the Q2 2021 earnings call.

“I can't predict that that's what's going to happen. But there is not a lot of great inventory out there. Inventory is declining. And we have some of the best inventory out there. And then, one, it's generally underpriced. So when we get big increases, it still looks good.” - David Zaslav

Brand Moat (Strong and growing)

A business with a brand moat has phenomenal top-of-mind loyalty with its consumers. In this situation, customers go out of their way to purchase its products and services despite other options and are often willing to pay a premium.

WarnerMedia and Discovery both have excellent top-of-mind brand recognition across the world. Its main movie studio, Warner Bros, was founded in 1923 and has since become one of the world’s leading entertainment studios. The iconic WB logo is prominently displayed before the start of all of its movies and has formed deep emotional connections with audiences. Warnermedia has many other iconic brand names such as HBO, CNN, DC, Cartoon Network, Cinemax, and TNT.

It is impressive that over 74 million people subscribe to HBO Max after only starting in mid-2020. This performance is despite the unfortunate fact that the business is limited internationally. For example, it cannot enter the UK, Germany, or Italian markets due to the myopic managerial decision in 2019 to renew a multi-year licensing deal with Comcast’s Sky. This stellar performance is a testament to the superb brand power that it has cultivated.

Distributed in over 220 countries, Discovery has multiple top-of-mind international TV network brands such as the Discovery Channel, HGTV, Food Network, TLC, Animal Planet, Oprah Winfrey Network (OWN), MotorTrend, and many others. It has a trove of local language IP, enabling the company to form meaningful connections with customers in its markets. In the 2021 10K, Discovery claims that it has provided content to ~3.5 billion cumulative subscribers and viewers worldwide.

Management

David Zaslav, a Brooklyn native, is the company’s CEO. He has a long history in the media business. He spent 18 years at NBC, where he helped to found CNBC and MSNBC. In 2007 he became the CEO of Discovery and had since transformed the company from a pure cable broadcasting company into a content creation company. He also orchestrated the 2018 Scripps merger that bolstered its offering with complementary networks in multiple essential categories.

This situation was similar to the AT&T deal since Discovery leveraged itself to a 5x Debt to EBITDA to execute the purchase. The management team predicted it would de-lever to 3.5x with $350 million in cost synergies in two years. Zaslav and his executive team over-delivered. They achieved this goal in less than a year and captured more than $1 billion in cost savings, or ~3x their original target. John Malone, a legend in the cable media business and board member of WBD, has mentored Zaslav and taken him under his wing. The fact that such a rockstar in the industry has deep confidence in the CEO is encouraging.

Compelling Reasons for Long-Term Ownership

Remarkable Library of Valuable Assets

Warner Bros Discovery has evolved into a premium media and entertainment IP giant. It owns, co-produces, and has rights to major international films, binge-worthy tv shows, multi-year live sports rights, national/local networks, and more. The merger was a great fit since both sides had what the other needed. For instance, Discovery is the leader in the niche market for unscripted shows, with a reach of more than 80 networks in over 200+ countries. WarnerMedia, on the other hand, possessed several powerhouse brands with a leading Hollywood movie production studio while lacking the international reach of Discovery (due to reasons I’ll describe later).

The company plans to fold its two streaming services, HBO Max and Discovery+, into one product. This streaming service will be a behemoth in the market that will be difficult for households worldwide to ignore. It is like having a Blockbuster at your fingertips for the cost of a few cups of Starbucks coffee. Although Netflix and Amazon Prime are two industry heavyweights, the depth and breadth of their exclusive content pale in comparison to what the new HBO Max will offer. They also do not have the same decades of experience in the media and entertainment industry as WBD. The salient difference here is that WBD has its roots as a media content generation company. In contrast, Netflix and Amazon Prime started purchasing rights from suppliers and vertically integrated backward into media production. Despite some recent success with winning awards, shifting into this new business is hard to execute and is not necessarily within its circle of competence.

Insider incentives

It is a positive signal that John Malone, who has a long history of success in the media and telecom industry, ultimately endorsed the deal. Before the merger, he owned 20% of the voting rights despite owning < 1% of the equity of the pre-merger Discovery. Thus, Malone had the power to block the reclassification of Discovery’s stock, which was an integral part of the agreement. He did not impede the deal or ask for additional compensation for converting shares into a single WBD stock class structure that would drastically reduce his voting control. This accommodation was not charity work. The Cable Cowboy himself went on CNBC and said he sees this unification as a tremendous win for shareholders. He ultimately believes that this event is a catalyst for HBO Max to have international DTC success through the extensive distribution reach of Discovery.

It is essential to look at insider actions and incentives before investing in a business. Fortunately, WBD’s management and insiders have aligned themselves with shareholders through equity ownership. First off, management is purchasing stock from the open market. For example, on April 27th, Zaslav and his CFO, Gunnar Wiedenfels, purchased a combined 75k shares at ~$1.5mm. Additionally, the board of directors has highly incentivized the CEO and his management team with lucrative options and equity compensation packages. For example, Zaslav was paid an annualized $74.67 million in 2021. He was front-loaded $202mm in stock options over 6.5 years ($31mm per year). In addition to the options, he was paid $43.67 mm ($3 mm base salary + $13.165 mm stock awards + $22 mm cash performance awards + $1.1 mm other + $4.4 mm bonus). The vast majority of his options have escalating strike prices greater than the initial stock price of ~$24. While the compensation is generous, the value of his package will substantially decrease unless he creates shareholder value that manifests itself through the stock price (granted, he has until 2025/2028 to make it happen). If he doesn’t move the needle over the next six years, his true compensation is a fraction of what the board originally gave him.

While the other C-suite executives are not paid as much as Zaslav, they still own a sizable WBD equity value relative to their annual pay.

Pricing Power

The merger augmented the pricing power that the business has with its TV distributors and advertisers. Discovery already had 20% of the total viewership with its MVPD affiliates. The total viewership will surely increase now that the company has acquired leading networks like TNT, TBS, CNN, Cartoon Network, and Adult Swim. This increased scale will enable them to negotiate better carriage deals since the distributors do not want to lose those networks. Additionally, the threat of a superior and fast-growing DTC revenue stream further increases WBD’s leverage since it is no longer entirely dependent on legacy distribution.

On the advertising front, management notices a level of demand from advertisers that have exceeded their expectations. On an earnings call, the CEO mentioned that more than 800 advertisers purchased inventory on their platform, more than 4x their original target for Q2 2021. Zaslav explained the rationale for the increase in demand.

“Premium online video inventory is scarce in the first place because a lot of the viewership is happening on ad-free platforms, that drives super high demand and a hot market environment right now. - David Zaslav

Additionally, the new OTT product enables the company to sell more sophisticated targeted ads to customers. This 1:1 level of customization allows them to sell that ad space at a premium to the traditional product. For example, Discovery currently offers an ad-light tier that generates an $11 ($5 sub fees + $6 from advertising) monthly US ARPU with only three minutes of advertising. For linear, on the other hand, the business is receiving a mere $7 ($3.5 sub fees + $3.5 advertising ). Now that the unique value proposition is significantly increasing post transaction, they should see a step up in demand from other businesses wanting to target its highly engaged audience on its platform.

Possible Take-Over Catalyst down the Road

The competition is heating up with Netflix, Apple, Amazon, Disney, Paramount, NBCUniversal, Hulu (owned by Comcast and Disney), and Warner Bros Discovery competing for subscribers. Content is king. Audiences demand a product that consistently provides thrilling entertainment. These participants all have an eye on the prize and must continuously spend to attract customers and minimize churn. Therefore, a company must produce enough revenue through a large subscriber base to sufficiently offset these fixed costs to attain profitability. The logical next step is for the fragmented environment to continue to consolidate.

The WarnerMedia/Discovery deal has paved a path forward for future M&A activity. When Warner spun off from AT&T, it released itself from the regulatory constraints that plagued its former parent. For example, Trump’s DOJ challenged the AT&T and Time Warner merger in the court system for anti-trust reasons. As we have learned from history, government scrutiny often occurs when a distributor also owns cable networks. Now that it has broken off and merged into Discovery via a Reverse Morris Trust, a major pure-play media content company has emerged with extraordinarily valuable assets. The stars are aligning for WBD to either get bought out at a premium or for itself to acquire a subscale player once management successfully hits its leverage target.

Risks and Rebuttals

Leveraged Balance Sheet

On consummation of the union, WBD sent AT&T $40.4 billion in value that was debt-financed. Post-transaction, WBD now has ~$56.4 billion in leverage ($14.8B existing + $41.6B from the $T deal). At ~$6 billion in estimated 2023 FCF, there is a risk that it will not be able to service the debt effectively. Additionally, aggressively paying it down could impede its ability to invest in new content. Management signaled that it would aggressively de-lever and estimated that the business would devote 20% of unlevered free cash flow to interest payments and 50% to principal payments through 2024. With a blended interest rate of roughly 4.41%, the business is on the hook for $2.5 billion in annual payments. This cost is a significant drag on the bottom line. Furthermore, if it does not sustain enough free cash flow after increasing its content investments, there could be pressure to reduce film and tv show budgets. This pullback could impede its growth prospects.

Rebuttal: FCF Machine and Disciplined Management

WBD is a free cash flow machine with over $6 billion in sustainable cash flow that includes $3 billion in synergies from cost avoidance. David Zaslav’s track record speaks for itself. He has already proved his ability to deliver on quickly reducing leverage through the Scripps deal. Management has clearly outlined its plan to aggressively pay down the debt and lower the debt servicing costs.

Fortunately, there is a ton of low-hanging fruit from eliminating duplicated corporate functions and various lousy capital allocation decisions from WarnerMedia, such as the rich $1 billion investment in a floundering CNN+. There is a good possibility that the estimate is reasonably conservative. For example, there is around $6 billion in technology and marketing expenses between the two distinct platforms. A portion of that is unnecessary in the future.

The business’s projection of synergies also does not include potential revenue-related synergies that may have significant upside. Opportunities such as cross-promotion/marketing, joint project development, and the ability to unlock new content franchises across its vast library of iconic IP may bring in more revenue than either company could get on its own.

Declining Linear Revenues

Discovery’s management projected that its US and Internationally linear revenue would decrease at an annual rate of 4% and 3%, respectively, through 2025. In 2021 alone, its total US networks portfolio subs declined 8%. While this is a known secular consumer shift that has been known for years, cable and network companies are quickly losing their primary stream of revenue. It is the brutal reality of creative destruction through capitalism. While WBD is decoupling from traditional OTA (Over the Air) distribution methods, it is still a substantial portion of its sales. For instance, in 2021, the company raked in ~$12.6 billion in DTC sales ($1.6B from Discovery and $11B from WarnerMedia). This new and exciting revenue stream represents only about a quarter of total revenue. Thus, those declines in linear subs will have an outsized negative effect on performance. In reality, revenue growth from DTC may ultimately cannibalize linear revenues. Also, since distribution agreements have a limited term, there is no guarantee that the business will be able to negotiate favorable contracts. If the cable broadcasting industry continues to consolidate, there could be further headwinds on future per capita affiliate fees.

Rebuttal: DTC adds will more than offset cable declines

While there are significant industry headwinds right now regarding cable-cutting, the DTC adds are value-added and not just cannibalistic. The ARPUs for OTT subs are much higher than from its traditional business. For its ad-light tier, for example, Discovery+ makes $11 a US subscriber from a $5 monthly fee and over $6 in advertising for only 3 minutes of ad time vs. $7 from linear. Zaslav was seemingly unconcerned with losing cable customers, “If we lost a million [cable] subs…all we need to do is pick up 650,000 [streaming] subs in order to be making more money.” Warner’s ARPUs are even higher at ~$10 per sub. As long as the company maintains its competitive advantage and can hit its subscriber growth targets, margins should increase.

Past Licensing Deals Threaten Global Expansion

The shortsighted decision of WarnerMedia’s previous regime to sell its international rights to Sky is a significant reason why this transaction was crucial. That licensing deal makes Comcast’s subsidiary the exclusive home of HBO in the UK, Germany, and Italy until 2025. It also cannot launch in France until the expiration of its contract with OCS at the end of 2022. Fortunately, Discovery kept its international rights. This flexibility enables the combined streaming platform to compete globally while waiting for the exclusive deals to unwind.

HBO has had a deal with Sky since 2010. Maybe a less obvious but problematic issue is HBO is virtually a white label product for the company. An article about the arrangement spoke to this problem.

Due to past licensing deals, HBO Max could face additional marketing challenges. While Sky has advertised itself as the “Home of HBO,” many British viewers don’t know the HBO brand well because it doesn’t operate as an independent channel on Sky’s pay-TV service as it does in the U.S., Godard said. Instead, HBO shows like “Game of Thrones” air on Sky Atlantic, which features a mix of American programming. “The bulk of viewers would first think of Sky, not HBO.” - L.A. Times

HBO has a brand positioning problem in several European regions. Once those rights release back to WBD, it will most likely need to spend extra marketing dollars to gain a foothold in the minds of its customers.

Rebuttal: Discovery’s international presence will partially offset the limitation

There is no question that this is not an ideal scenario. Not having the rights will initially impede the international subscriber growth of the company. In the meantime, the business can make inroads into the market with its Discovery assets. It will also have time to form a genuinely compelling synthesized product ready to go with potentially another merger between now and then. Furthermore, consumers develop emotional ties to the stories and featured characters more than the brand that distributes or produces them. Once the rights come back, consumers will gravitate toward their favorite movies and tv shows packaged into one service.

Content Spend Treadmill

There is a never-ending content spend treadmill as competition is heating up. Consumers need more and more to justify paying $100 - $240 per year for one subscription. For example, on a cash basis, Netflix and WBD spent $17.14B and $15.39B (pro forma), respectively, in 2019. In 2021, Netflix’s increased its investment 33% to $22.8 billion ($17.33B cost of revenue + 5.47B cash addition to content spend over amortization) and WBD spent close to an estimated $20 billion (+30%). For example, on the recent WBD Q1 2022 earnings call, management was surprised at how much WarnerMedia’s management was spending. Due to “previously unplanned projects,” the CFO estimated that the profit baseline from the originally published pro forma numbers is “around $500 million less than expected.” Despite over $40 billion in sales from WarnerMedia, there is essentially no free cash flow. The industry is starting to realize that this dynamic is not sustainable for shareholders over the long run. For instance, Zaslav asserted the importance of a disciplined approach, “We plan on being careful and judicious. Our goal is to compete with the leading streaming services, not to win the spending war.” Likewise, on the Netflix Q1 2022 earnings report, the company revealed that it lost 200k net subscribers. In response to this downturn, the CFO conveyed that it would be pulling back some of its content expenditures. This stance is an overreaction and misses the mark. Audiences want more compelling content, not less. The solution is to reach a critical mass that will enable a business to spread its fixed costs over a larger revenue base. A streaming company will need to reach an inflection point where the next dollar spent on media is no longer necessary to attract more subscribers.

Rebuttal: Robust Library, Increasing Scale, and Disciplined Management

As mentioned earlier, WBD is a media and entertainment production company that has developed a phenomenal library of high-quality assets with an expansive international presence. WBD holds all of the cards. Executives from other companies will surely come calling when they realize that they cannot make it on their own. An acquiring business will need to pay a premium to effectuate a deal. Alternatively, WBD will continue to scale up through further acquisitions of valuable assets.

Zaslav and (especially) John Malone both have a stellar track record of shareholder-friendly deal-making and industry experience to pull this off. While there was a negative operating expenditure surprise on the latest Q1 2022 earnings report from the WarnerMedia side, the executive team has identified “a lot of chunky investments” that are lacking an adequate ROI profile. Management is laser-focused on disciplined spending and eradicating the bad projects started by the prior regime. Once this occurs, operating margins will expand and free cash flow will improve.

Execution Risk

Success in bringing together two cultures is not a foregone conclusion. Recently known as a turnstile for CEOs with four different execs at the helm over four years, WarnerMedia comprises highly protective siloed businesses and big-budget Hollywood movies. On the other hand, Discovery is a cable business known for its thrifty unscripted material. With only a few WarnerMedia execs remaining post-merger, Zaslav’s officers from Discovery are leading most of the business units of the newly formed entity. Promising $3 billion in synergies from cost avoidance, the CEO will have to make many challenging decisions that could destabilize the organization and neuter its creative prowess.

Rebuttal: Zaslav is the right man for the job

There are countless reports of Zaslav hitting the ground running in effectuating a successful marriage. He purchased a home in Beverly Hills from movie producer Robert Evans to immerse himself in Hollywood. According to Business Insider, the media mogul began doing his homework to learn the culture and devise a plan many months leading up to the deal's closing.

“Zaslav has been canvassing Hollywood players about their peers, digging deep into Warner fiefdoms and dysfunctions to understand the storied studio's challenges, and learning what makes creatives tick. His top priorities will be preserving pre-pandemic businesses — including restoring Warners' damaged relationship with theater owners and talent — and shaking up WarnerMedia's entrenched culture of silos, while also marshalling the force of a major new player in the streaming wars.” - Business Insider

He ultimately has a reputation for having a less formal yet more collaborative and accountability-demanding approach to running a company. With the support of John Malone and years of substantial leadership experience in the industry, this strategy should yield positive results.

Valuation

Pro Forma Enterprise + Equity Value

I triangulated the intrinsic EV using a 13x EV/EBIT multiple (based on the lower end of the industry average over the past decade using comp data from NYU Stern over the past decade), a DCF calculation, and an 8 Year EBIT payback time. The mean of the valuation methods is $57.28 EV per share or $35.51 with a 38% MOS. Subtracting net debt translates to a target buy price of $19.09.

Furthermore, if we look ahead to 2024, management projects that it will reduce debt to $42B or 3x 2024 management’s projected adjusted EBITDA ($14B). I adjusted this figure upward to $45B for conservatism by adding $3B in debt. Net Debt is $27.13B or $11.28 per share after accounting for $17.81B in projected excess cash + investments. With projected growth expectations and $3B in synergies, normalized 2024 EBIT is $14.59B. At 13x, the 2024 EV is $78.89 per share with a 2024 equity value of $67.61 per share. This represents a 272% premium over today’s price.

What do you think? Comment below if you agree or disagree with my thesis or if you have any other thoughts to share.

Please do your homework. This article is for education and entertainment only and should not be taken as investment advice.

FY 2022 Pro Forma Estimated. Defined as EBITDA - Maintenance Cap-Ex.

EBITDA = Operating Earnings + Amortization of Film and television costs + Depreciation & Amortization.

Maintenance Cap-Ex = 80% of total cap-ex, including all cash content spend.

Traditional TV via subscription to cable, satellite services, or through over-the-air broadcasts